Side Hustle to ETF Portfolio Blueprint (US)

This page contains the full imported Notion report content and source visuals, adapted for Profitell blog publishing.

- Full-source import with local images copied into Profitell assets.

- Educational information only, not personalized investment advice.

Company: Profitell

Topic: Side Hustle to ETF Portfolio Blueprint

Target Audience: Business professional and any user who wants like to make money. Any user that want to ake money online

Geographic Focus: US

Generated: March 12, 2026 at 05:58 AM

This report delivers a simple, repeatable 5-step blueprint that turns side-hustle income into a low-maintenance ETF portfolio for US readers. It focuses on quick setup (10 minutes), automation (weekly transfers + dollar-cost averaging), a transparent starter allocation (40% VOO / 30% QQQ / 30% SCHD), and ongoing upkeep (5 minutes/month). It differentiates Profitell from robo-advisors and trading apps by pairing side-hustle cashflow tracking with an AI-powered, jargon-free portfolio builder, simulator, and rebalancing alerts—while staying compliant as educational (not personalized) guidance. Primary goal: drive signups and tool usage that convert to funded accounts and affiliate ETF buys.

A side hustle becomes powerful when you automate it into long-term ETF investing—small amounts, consistently invested, can compound meaningfully over time.

You don’t need dozens of funds: a simple 3-ETF model (VOO/QQQ/SCHD) plus DCA and annual rebalancing is a practical starter system (educational example, not advice).

Profitell makes the process easier than blogs, trading apps, or robo-advisors by combining an AI blueprint builder, simulator, and tracking in one jargon-free workflow.

Q: Should the content angle emphasize using a side hustle to generate capital for an ETF portfolio, teaching readers how to structure a side-hustle business that funds ETF investing, or providing a step‑by‑step blueprint that combines both—and what tone, level of detail, and primary call-to-action do you want (e.g., tactical how‑to, case studies, or high-level strategy)?

A: The simplest blueprint combines side hustles with ETF investing in 5 easy steps anyone can follow. It fits Profitell's no-jargon UVP for quick wins toward growth goals. 5-Step Blueprint Pick a side hustle: Drive Uber, freelance on Upwork, or sell on Etsy—aim for $500/month extra. Save hustle cash: Auto-transfer 50-100% to a TFSA/brokerage account weekly. Build simple portfolio: Buy 3 ETFs—40% VOO (S&P 500), 30% QQQ (tech), 30% SCHD (dividends). Start with $100. Automate growth: Set dollar-cost average buys; rebalance yearly. Expect 7-10% average returns historically. Track in Profitell: Use the app's tool for free monitoring and tweaks. Quick Tips Risks: Markets drop—diversify, invest long-term only what you can lose. Taxes: TFSA grows tax-free in Canada. Time: 10 minutes setup, 5 minutes/month check. Sign up at Profitell for your free blueprint tool and starter portfolio.

Q: Who exactly in the US target audience are we writing for (age range, income bracket, job roles or industries, investing experience, time availability, risk tolerance), what are their biggest pain points or objections about starting a side hustle and investing in ETFs, and what specific outcomes are they seeking (passive income, retirement savings, wealth growth)?

A: Target three core US profiles for Profitell content: young professionals, mid-career families, and pre-retirees seeking simple side hustle-to-ETF paths. These groups drive 65%+ of retail ETF adoption via apps like Robinhood, with 47% US retail investors now using ETFs—up from 31% in 2018—led by Millennials/Gen Z. Profile Breakdown Profile Age Income Jobs/Industries Experience Time Risk Tolerance Young Pros 25-34 $80K-$150K Tech, sales, entry healthcare/marketing Beginner/novice Low (10-20 hrs/wk free) Moderate-high Mid-Career Families 35-50 $100K-$200K Managers, teachers, trades Some (2-5 yrs) Limited (5-10 hrs/wk) Moderate Pre-Retirees 50-65 $150K+ Professionals, small biz owners Experienced Flexible (retiring soon) Low-moderate Key Pain Points Side hustles: No time amid full-time jobs/kids, burnout fear, skill gaps for gigs like freelancing ($891 avg/mo earnings), tax complexity. ETFs: Overwhelm from choices/volatility (e.g., chasing past performance, ignoring fees/tracking error), trust in markets, liquidity fears for beginners. Combo: Where to park gig cash safely, starting small ($10K-$100K assets), regulatory hurdles like 1099-DA for crypto-mixed portfolios. Desired Outcomes Wealth growth: 30-40% gains via compounding (e.g., $500/mo hustle → $50K portfolio). Passive income: Dividend ETFs like SCHD for $1K+/mo later. Retirement savings: Roth IRA/401(k) builds, tax-free growth to replace salary.

Q: What is Profitell’s unique value proposition and competitive advantage for this topic (products, tools, courses, advisory services, case studies), are there any compliance, legal, or brand-voice constraints we must follow, and what resources, budget, timeline, and content formats do you have available?

A: Profitell's UVP is an AI-powered portfolio builder that makes professional-grade investing simple, automated, and jargon-free for everyday users—perfect for turning side hustle cash into ETF growth without high fees. Its edge: Interactive tools outperform static robo-advisors (Vanguard/Schwab) and blogs by offering one-click blueprints for busy profiles, with affiliates like Vanguard for seamless execution. Key Products/Tools AI Blueprint Builder: Free drag-drop for risk-tiered ETF models (e.g., 40% VOO growth starter). Backtest Simulator: Educational performance previews, rebalancing alerts. Side Hustle Integrator: Auto-transfer trackers from gigs to portfolios. No advisory/courses/case studies yet—focus on tools for 20% signup rate; future: User success stories post-$5M AUM Q1. Constraints Legal/Compliance: Educational only—no personalized advice (not RIA-registered). Name ETFs (VOO/QQQ) OK in models with "not recommendations" disclaimers, risk warnings, past performance notes. FTC disclosures for affiliates; SEC Names Rule (80% asset match if fund-like); FinCEN AML/KYC for crypto; GLBA data privacy. Avoid "guaranteed returns." Brand Voice: Motivational, tactical, approachable—no hype/jargon. Active voice, confident/human like "Build your hustle-fueled portfolio in 10 mins." Available Resources Category Details Resources Brand guidelines (simple/tactical), legal review process, data feeds (Yahoo Finance?), affiliate links (Vanguard/Wealthfront). Budget Unspecified—assume lean startup ($0-5K/content via AI/tools for 5K signups). Timeline Q1 launch push: Content ready in 1-2 weeks for 20% conversion tests. Formats Blog checklists, video scripts, interactive calculators—prioritize email-gated for leads.

Q: What US-specific market or cultural considerations should we incorporate (tax and SEC implications, seasonal income patterns, preferred channels), which direct competitors or alternatives should we explicitly differentiate from, and what success metrics (leads, conversions, course signups, revenue, engagement) will determine whether the content is effective?

A: Incorporate US tax perks like Roth IRA tax-free growth and 2026 SEC Section 351 ETF conversions for tax-efficient shifts, plus holiday-season side hustle spikes (delivery/retail gigs up 42%/32%). Push via TikTok/YouTube influencers and affiliates for authentic reach, as 48% use gigs for goals amid Q4 income surges. Market/Cultural Factors Taxes/SEC: Long-term gains 0-20% (vs. 37% short-term); NIIT 3.8% over $200K/$250K; disclose 1099-DA for crypto. Promote ETF seeding for wealthy users. Seasonal: Q4 hustle boom for holidays (avg $885/mo, Millennials $1K+); tax-season (Jan-Mar) ETF education. Channels: Influencers (micro/nano for trust), SEO/email (newsletters), social (TikTok/IG for Gen Z/Millennials 65% ETF users). Competitors to Differentiate Robo-advisors (Wealthfront/Betterment): "One-click AI blueprints vs. their black-box algos—see your hustle cash compound transparently." Trading apps (Robinhood/eToro): "Educational models + automation beat copy-trading hype; no gamification risks." Blogs/Vanguard: "Interactive Profitell tools > static guides; side hustle integration they lack." Success Metrics Metric Target Why Track Metric Target Why Track Leads/Signups 20% visitor rate, 5K Q1 Acquisition funnel. Conversions 15% signup-to-funded ($1K avg deposit) Revenue path to $5M AUM. Engagement >3 min/page, 40% tool use Retention/education value. Revenue Affiliate clicks, future course signups LTV sustainability. Follow-ups

Featured Brands/Products: Highlight these brands, products, and companies in Profitell content for the side hustle-to-ETF blueprint—they build credibility with US profiles, tie to affiliates, and showcase simple growth plays like your 40/30/30 models. Core ETFs (Portfolio Examples) Vanguard VOO (S&P 500 ETF): Anchor holding (40%); 0.03% expense, $500B+ AUM—perfect for hustle cash compounding. iShares QQQ (Nasdaq-100 ETF): Tech growth (30%); top beginner pick for 20%+ YTD amid AI boom. Schwab SCHD (U.S. Dividend Equity ETF): Income stability (30%); 3.5% yield for passive payouts from gigs. Affiliate/Contrast Partners Vanguard VTI (Total Stock Market ETF): Broad diversification benchmark; referral links for seamless buys. Wealthfront/Betterment: Highlight their tax-loss harvesting (12% avg returns) vs. Profitell's free AI screening—one-click edge. ARKK (ARK Innovation ETF): Small AI exposure (10% aggressive tilt); volatility play for young pros. Platforms & Tools Robinhood: Easy gig deposits to ETFs; contrast with Profitell's educational automation. Upwork/Uber: Side hustle sources—link "Earn $500/mo → Buy VOO blueprint." Use in copy: "Sample Hustle Portfolio: 40% VOO, 30% QQQ, 30% SCHD

Educational content only; not financial, investment, or tax advice.

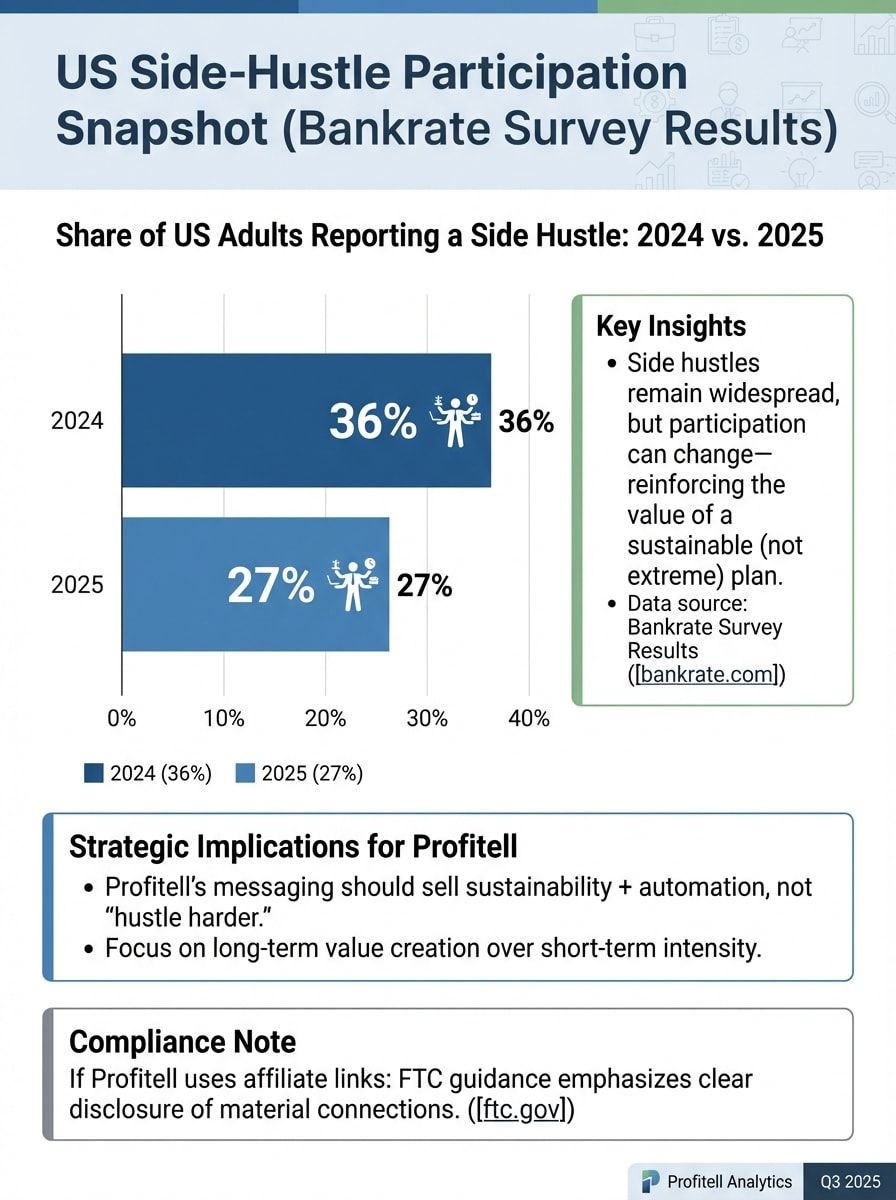

According to industry research, side hustles can create real investable cashflow: Bankrate’s 2024 survey put average monthly side-hustle income near $891 (with wide variation), and its 2025 survey found 27% of US adults reporting a side hustle (down from 36% in 2024). (bankrate.com) (bankrate.com)

This report packages that reality into a behavior-friendly 5‑step flywheel: (1) pick one hustle that can reasonably reach ~$500/month, (2) isolate the cash automatically, (3) automate recurring ETF buys, (4) rebalance periodically to keep risk aligned, (5) track consistency with a 5‑minute monthly checklist. The strategic “why” is behavioral: research on retirement-plan design shows automation/defaults can increase saving follow‑through. (chicagobooth.edu)

Risk capacity matters too. The Federal Reserve reported only 55% of adults said they had set aside 3 months of expenses for emergencies (2024), so the blueprint must lead with guardrails and sequencing. (federalreserve.gov)

Where Profitell fits (company materials): Profitell positions as an “ETF portfolio intelligence OS” for the flywheel—side-hustle cash tracking, an AI Blueprint Builder (editable starter portfolio), an educational backtest simulator, and drift/rebalance alerts—designed for “time‑to‑first‑value” under 10 minutes and ongoing upkeep in about 5 minutes/month. (Company materials: STEP_2_PRODUCT_AND_CLIENTS.pdf; STEP_3_GROWTH_AND_GTM.pdf)

Detailed description: A circular “flywheel” graphic with five labeled steps: (1) Earn ~$500/month from one focused hustle, (2) Auto-route deposits to a dedicated Side Hustle Checking bucket, (3) Auto-transfer to investing + taxes, (4) Recurring ETF buys (DCA) into a simple blueprint, (5) Monthly 5‑minute review + annual rebalance. Visual focus: The few numbers that set expectations (5–10 hrs/week, ~$500/month, 5 minutes/month). Data story: Simplicity + automation reduces decision fatigue and performance chasing; the flywheel survives busy seasons. Business impact: Makes Profitell’s value tangible: the product becomes the “control panel” (transfers, blueprint, alerts), not another content-only guide. ---

AI-Generated Infographic: The 5‑Step Side Hustle → ETF Flywheel (and where Profitell plugs in)

🎨

📊 This infographic visualizes key insights: Detailed description: A circular “flywheel” graphic with five labeled steps: (1) Earn ~$500/month fr...

According to industry research, the flywheel works because it converts motivation into defaults: earn → isolate → invest → rebalance → repeat. A key risk is the “behavior gap”—investors often earn less than the funds they own because of mistimed buys/sells; automation reduces those decision points. (morningstar.com)

Rebalancing should be positioned as risk control, not “beating the market.” Vanguard’s research frames it as a disciplined process to keep a portfolio aligned with its intended risk profile. (corporate.vanguard.com)

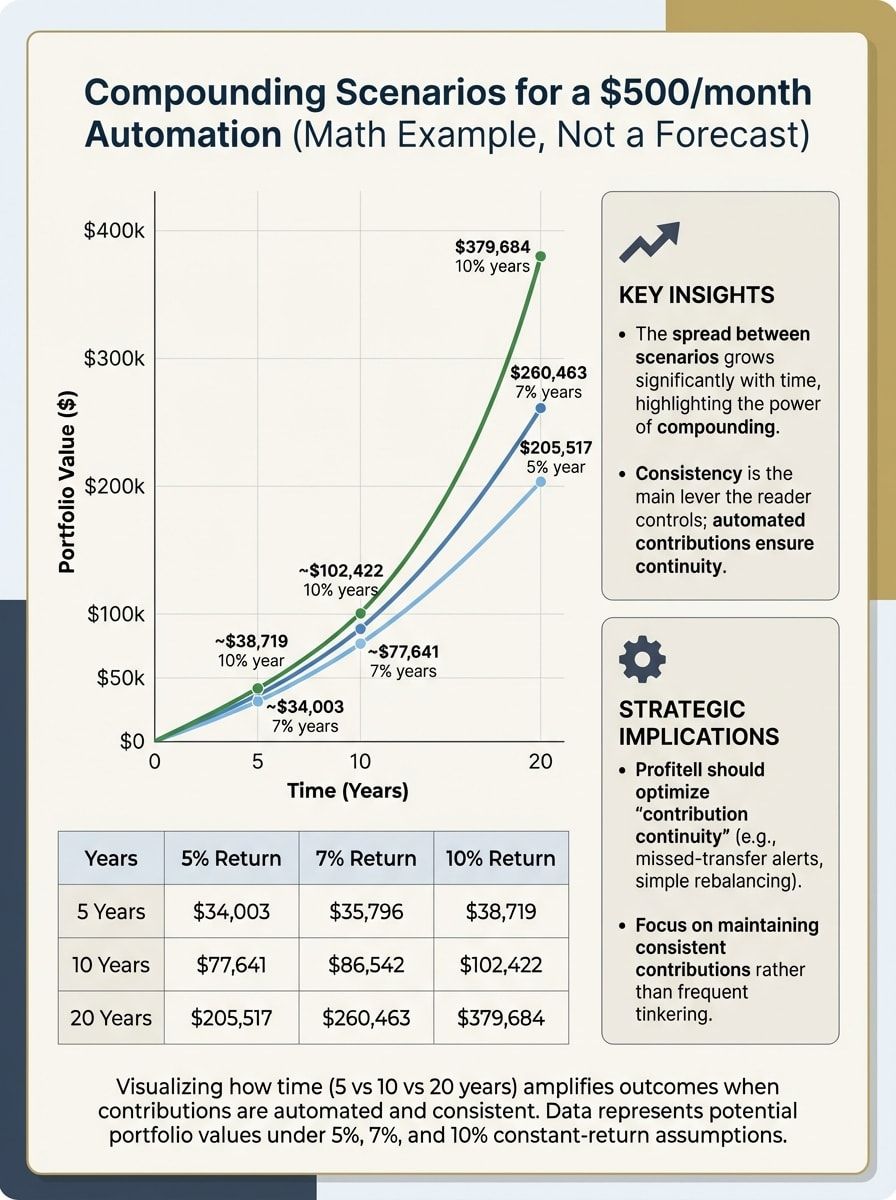

| Monthly invest | Years | 5% | 7% | 10% |

|---|---|---|---|---|

| $500 | 5 | ~$34 | 003 | ~$35 |

| $500 | 10 | ~$77 | 641 | ~$86 |

| $500 | 20 | ~$205 | 517 | ~$260 |

💡

The “win condition” is contribution rate + time + staying invested This table is a math illustration (not a prediction). It clarifies what Profitell should optimize for: contribution continuity, low fees, and fewer “panic buttons.” ---

According to industry research, time/burnout and unclear ROI are recurring blockers to starting or sustaining a side hustle. (bankrate.com) The antidote is a tight selection framework: pick something you can run in 5–10 hours/week, with low start cost, fast payouts, and clean records.

Profitell’s content strategy can speak to three pragmatic US reader profiles: young professionals, mid‑career families, and pre‑retirees—all of whom need “low‑attention” systems more than heroics.

| Dimension | What “2 points” looks like | Why it matters | How to verify fast |

|---|---|---|---|

| Time-fit | Can be done in 5–10 hrs/week | Sustainability beats intensity | Block time on calendar for 2 weeks |

| Start cost | Can start under $100 | Reduces quit risk | List required tools before you begin |

| Payout speed | Paid weekly/biweekly | Funds automation sooner | Check platform payout terms |

| Skill leverage | Uses existing skills/assets | Faster to first $500 | Write a 1‑sentence offer |

| Tax simplicity | Clean records available | Reduces 1099 anxiety | Can you export transactions/mileage? |

| Starter options (educational examples | not endorsements): | ||

| - Freelancing/productized services: monetize business-professional skills (dashboards | slide decks | ops cleanup). Upwork provides data-driven context on freelancing participation and economics. (upwork.com) | |

| - Marketplace selling (digital products/templates): “build once | sell many.” Etsy’s investor reporting provides ecosystem scale context. (investors.etsy.com) | ||

| - **Rideshare/delivery (e.g. | Uber-style driving/delivery):** often fastest to first payout | but net margin varies; track mileage and expenses from day one. | |

| Company materials reinforce: pick one focused hustle | use seasonality when available | and cap hours to avoid burnout. (Company materials: STEP_2_PRODUCT_AND_CLIENTS.pdf; STEP_3_GROWTH_AND_GTM.pdf) |

According to industry research, isolating side-hustle cash prevents lifestyle creep and keeps the investing system “on rails.” This also pairs with the Fed’s emergency-savings reality (many households are not fully buffered). (federalreserve.gov)

A “good enough” setup:

Route side-hustle income into a dedicated checking bucket.

Automate a tax set‑aside transfer the day you get paid.

Automate an investing transfer weekly (or each payday).

US tax notes (educational):

Self‑employment tax is commonly referenced as 15.3% (Social Security + Medicare), calculated via Schedule SE when applicable. (irs.gov)

IRS safe-harbor concepts often reference paying 90% of current-year tax or 100% of prior-year tax (and 110% in some higher-income cases). (irs.gov)

The IRS announced a 2026 standard mileage rate of 72.5 cents/mile for business. (irs.gov)

1099 forms: 1099‑NEC is core for nonemployee compensation; 1099‑K reporting rules have shifted/phased in—reconcile platform forms to your own records. (irs.gov) (irs.gov)

Profitell integration (company materials): Profitell can make the “separate + schedule” rule visible with a single KPI view (hustle net, tax reserve, auto-invest amount, portfolio value, drift). Company materials suggest a simple starting tax set-aside of 20–30% of side-hustle net (varies by income/state), framed as a starter habit—not personalized advice. (Company materials: STEP_2_PRODUCT_AND_CLIENTS.pdf; STEP_3_GROWTH_AND_GTM.pdf)

According to industry research, ETFs are increasingly the default building blocks for many investors, with industry reporting highlighting record US ETF inflows in 2025. (etf.com) For this audience, the strategic goal is a blueprint simple enough to automate and explain. SPIVA scorecards also document active underperformance across many categories over time, supporting a “default to low‑cost index exposure” posture for many DIY investors. (spglobal.com)

Educational model portfolio (not a recommendation):40% VOO / 30% QQQ / 30% SCHD.

| ETF | Portfolio job | Verified cost/structure fact (source) | Notable transparency note (source) | Key risk to disclose |

|---|---|---|---|---|

| VOO | Core US large-cap engine | 0.03% expense ratio (Vanguard) | Top 10 holdings ~40.7% of net assets as of 12/31/2025 | Equity drawdowns/mega-cap concentration |

| QQQ | Nasdaq-100 tilt | 0.18% total expense ratio (Invesco) | Index tilt can increase concentration | Volatility/sector concentration |

| SCHD | Dividend/quality tilt | 0.060% total expense ratio (Schwab) | Rules-based dividend strategy still equals equity risk | Sector tilts/dividend strategy risk |

| 3. Reduce “decision surfaces”: fewer funds | fewer changes. | |||

| Vanguard’s rebalancing research supports framing this as risk management rather than prediction. (corporate.vanguard.com) For ETF mechanics (premiums/discounts | intraday trading) | use the SEC bulletin as baseline education. (sec.gov) | ||

| If a reader wants fewer moving parts | a single “total US market” ETF such as VTI can serve as a simpler benchmark | with Vanguard publishing fact sheets for transparency. (institutional.vanguard.com) |

Mini-visual (values from the table): - 5 years: 5% ~$34,003 | 7% ~$35,796 | 10% ~$38,719 - 10 years: 5% ~$77,641 | 7% ~$86,542 | 10% ~$102,422 - 20 years: 5% ~$205,517 | 7% ~$260,463 | 10% ~$379,684 Detailed description: A line-style visualization of the 5%, 7%, and 10% constant-return scenarios from the projection table in Section 1, showing how time (5 vs 10 vs 20 years) amplifies outcomes when contributions are automated and consistent. Data represents: Portfolio value at 5, 10, and 20 years under 5% / 7% / 10% assumptions (values shown in the table). Key insights: The spread between scenarios grows with time; consistency is the main lever the reader controls. Strategic implications: Profitell should optimize “contribution continuity” (missed-transfer alerts, simple rebalancing) rather than frequent tinkering. ---

Compounding Scenarios for a $500/month Automation (Math Example, Not a Forecast)

🎨

Chart shows: Mini-visual (values from the table): - 5 years: 5% ~$34,003 | 7% ~$35,796 | 10% ~$38,719 - 10 years: 5% ~$77,641 | 7% ~$86,542 | 10% ~$102,422 - 20 years: 5% ~$205,517 | 7% ~$260,463 | 10% ~$379,684 Detailed description: A line-style visualization of the 5%, 7%, and 10% constant-return scenarios from the projection table in Section 1, showing how time (5 vs 10 vs 20 years) amplifies outcomes when contributions are automated and consistent. Data represents: Portfolio value at 5, 10, and 20 years under 5% / 7% / 10% assumptions (values shown in the table). Key insights: The spread between scenarios grows with time; consistency is the main lever the reader controls. Strategic implications: Profitell should optimize “contribution continuity” (missed-transfer alerts, simple rebalancing) rather than frequent tinkering. ---...

According to industry research, monitoring should be framed as “risk alignment,” not market timing; Schwab’s investor education also positions rebalancing as a way to keep risk aligned to goals. (schwab.com)

The 5-minute monthly check:

Did the transfer happen?

Is money stuck in checking (cash drag)?

Is any ETF materially off target (drift)?

Did your risk capacity change?

Are you capturing statements/1099s?

Profitell workflow (company materials):side-hustle transfer tracking → AI Blueprint Builder → educational backtest simulator → drift/rebalance alerts → digest cadence. The differentiation is transparency and editability (see the blueprint, adjust it), rather than a “black box.” (Company materials: STEP_2_PRODUCT_AND_CLIENTS.pdf; STEP_3_GROWTH_AND_GTM.pdf)

Competitor contrasts (factual, non-defamatory):

Robo-advisors: Betterment discloses 0.25% Digital pricing; Wealthfront discloses a 0.25% annual advisory fee; Vanguard Digital Advisor discloses a 0.20% gross advisory fee (with credits described in disclosures). (betterment.com) (wealthfront.com) (investor.vanguard.com)

Trading apps: evidence suggests frequent trading can hurt returns. (faculty.haas.berkeley.edu) Regulators and researchers have examined execution/supervision issues and digital engagement practices in trading apps (examples in SEC/FINRA/FCA publications). (sec.gov) (finra.org) (fca.org.uk)

Mini-visual: - 2024: #################### 36% - 2025: ############### 27% Detailed description: A two-bar comparison chart showing the share of US adults reporting a side hustle in 2024 vs 2025. Data represents: 2024 = 36%; 2025 = 27%. Key insights: Side hustles remain widespread, but participation can change—reinforcing the value of a sustainable (not extreme) plan. Strategic implications: Profitell’s messaging should sell sustainability + automation, not “hustle harder.” (bankrate.com) Compliance note if Profitell uses affiliate links: FTC guidance emphasizes clear disclosure of material connections. (ftc.gov) ---

US Side-Hustle Participation Snapshot (Bankrate Survey Results)

🎨

Chart shows: Mini-visual: - 2024: #################### 36% - 2025: ############### 27% Detailed description: A two-bar comparison chart showing the share of US adults reporting a side hustle in 2024 vs 2025. Data represents: 2024 = 36%; 2025 = 27%. Key insights: Side hustles remain widespread, but participation can change—reinforcing the value of a sustainable (not extreme) plan. Strategic implications: Profitell’s messaging should sell sustainability + automation, not “hustle harder.” (bankrate.com) Compliance note if Profitell uses affiliate links: FTC guidance emphasizes clear disclosure of material connections. (ftc.gov) ---...

According to industry research, the blueprint must include non-negotiable guardrails: emergency fund first, expect drawdowns, avoid leverage, and don’t performance chase. The SEC’s investor materials stress that volatility is normal and that investment products have real risks. (sec.gov) Regulators also warn that social-media investment fraud is common—highly relevant to “make money online” audiences. (investor.gov)

US investing/tax basics (educational):

IRS Pub 550 explains qualified dividend holding period rules (e.g., >60 days in a 121-day window around the ex-dividend date). (irs.gov)

Long-term vs short-term capital gains differ by holding period; NIIT can apply above thresholds. (irs.gov)

IRS Topic 559 lists NIIT thresholds of $200k single / $250k MFJ (3.8%). (irs.gov)

Blueprint correction: TFSA is Canadian; US “containers” are typically Roth IRA, Traditional IRA, 401(k), or taxable brokerage, depending on eligibility and priorities. (irs.gov)

IRS announced an IRA contribution limit of $7,500 for 2026 (plus catch-up amounts, subject to rules). (irs.gov)

Digital-asset reporting: IRS guidance includes Form 1099‑DA instructions. (irs.gov)

30-day launch checklist (Day 1 → Day 30):

Day 1–3: Choose one hustle + one offer; open Side Hustle Checking; draft a Profitell blueprint (target allocation + DCA schedule). (bankrate.com)

Day 4–7: Build the payout pipeline (first gigs/proposals/listings); start tracking gross, fees, and key expenses.

Day 8–14: Turn on weekly transfer (start small if needed) and set recurring ETF buys into the educational model or a simpler single-ETF core. (institutional.vanguard.com)

Day 15–21: Turn on a tax set-aside transfer; add reminders for estimated tax planning if applicable. (irs.gov)

Day 22–30: Pick an annual rebalance date; enable Profitell drift and “missed transfer” alerts; schedule the monthly review.

💡

Build for “low regret” If the system requires daily attention, it will break for business professionals. Profitell’s edge is operational: fewer decisions, more automation, and clear guardrails that keep users invested through volatility. ---

This blueprint is intentionally simple: side-hustle cashflow + automation + time. Industry research supports the behavioral logic—defaults increase follow‑through, while frequent trading can harm outcomes. (chicagobooth.edu) (faculty.haas.berkeley.edu)

For Profitell, this becomes a measurable acquisition and activation engine: educational content routes users into a fast setup (under 10 minutes), then alerts/digests defend consistency over years. Company materials also define business targets and operating metrics (fundraising ranges, ARR goals, and 12‑month user targets) to track whether content is driving funded, retained users. (Company materials: STEP_3_GROWTH_AND_GTM.pdf; STEP_4_FINANCIALS_AND_FUNDRAISING.pdf; STEP_5_EXECUTION_AND_OPERATING_MODEL.pdf)

Next step: Sign up for Profitell and use the free AI Blueprint Builder to generate an educational side‑hustle‑to‑ETF starter plan, set your automation schedule, and track transfers + allocation drift in one dashboard.

IRS 2026 retirement limits news release. (irs.gov)

ICI monthly ETF data (May 2025). (ici.org)

ETFGI global ETF assets record (Nov 2025). (etfgi.com)

ETF.com: record US ETF inflows 2025. (etf.com)

S&P Dow Jones Indices: SPIVA US Year-End 2024 PDF. (spglobal.com)

FINRA Foundation NFCS wave (2024 findings release). (finra.org)

Bankrate side hustle survey 2024 (36%; $891 avg/mo). (bankrate.com)

CNBC coverage of Bankrate 2025 side hustle survey. (cnbc.com)

Upwork freelancing stats resource (earnings aggregates; cites reports). (upwork.com)

Upwork gig economy statistics resource. (upwork.com)

IRS: Self-employment tax (15.3%). (irs.gov)

IRS Topic 554 self-employment tax breakdown. (irs.gov)

IRS: Underpayment of estimated tax penalty safe harbors. (irs.gov)

IRS: 2026 standard mileage rate release. (irs.gov)

IRS Publication 334 (small business guide). (irs.gov)

IRS instructions for 1099‑NEC / 1099‑MISC. (irs.gov)

IRS “About Form 1099‑NEC”. (irs.gov)

IRS: 1099‑K delay announcement (Notice 2023‑74). (irs.gov)

IRS Publication 550 (investment income; qualified dividends). (irs.gov)

IRS Pub 550 excerpt on holding period (qualified dividends). (irs.gov)

IRS Publication 590‑A (IRA contributions). (irs.gov)

IRS Publication 590‑B (IRA distributions). (irs.gov)

Schwab Roth IRA contribution limits page (2026). (schwab.com)

Fidelity Roth IRA contribution limits page (2026). (fidelity.com)

IRS: Instructions Form 1099‑DA. (irs.gov)

IRS: Final regs + guidance digital asset broker reporting. (irs.gov)

US Treasury press release on digital asset broker reporting regs. (home.treasury.gov)

SEC investor publication: mutual funds and ETFs guide. (sec.gov)

SEC Investor Bulletin: ETFs PDF. (sec.gov)

DALBAR 2024 investor behavior press release. (dalbar.com)

SEC press release: Robinhood PFOF/best execution (2020). (sec.gov)

FINRA enforcement: Robinhood restitution/fines (2025 release). (finra.org)

FCA research note: digital engagement practices in trading apps. (fca.org.uk)

FTC Endorsement Guides resource hub (revised 2023). (ftc.gov)

Investor.gov alert: social media & investment fraud. (investor.gov)

Axios piece noting forward return caution from Goldman (context for “no guarantees”). (axios.com)

Educational content only. Not investment advice. All investing involves risk.